GreenFirst Forest Products (GFP): A Play On Lumber

GreenFirst Forest Products (GFP): A Play On Lumber

GreenFirst Forest Products, Inc. (GFP), is a fascinating company. GFP used to be called “Itasca Capital Ltd.”, and it was basically a holding company with a lot of cash and investments. After a successful investment into “1347 LLC” (now a fully owned subsidiary), Itasca found itself holding a lot of dry powder. In 2020 the company purchased a sawmill in Kenora, Ontario, at this point Itasca decided to change its name to GreenFirst Forest Products, to better reflect the new operations. In 2021 GFP acquired sawmill and paper mill assets from certain Canadian subsidiaries of Rayonier. The sawmills produce about 50% random length lumber, and 50% studs, as well as chips, shavings, and bark as by-products. In the past, the sawmills have shipped between 45-65% of their production to US customers while the remaining production is shipped to domestic customers. The paper mill manufactures paper-grade products that are used to print newspapers, advertising materials, etc. In addition to the mill assets, GFP also received logging right for 2.7m cubic meters of annual cut associated with the Ontario sawmills and 0.7m cubic meters associated with the Quebec mills. Lastly, GFP entered into several agreements with Rayonier including a chip supply agreement, a non-competition agreement, and a service agreement. The chip supply & service agreements expire around 2040, while the non-competition agreement ends in five years. The Rayonier acquisition was massive, GFP paid about $232.6m, in various forms of cash, stock, and debt. The costs were gargantuan for a company of GFP’s size (~$275m) - however, the acquisition was intelligent, making GFP one of the leading lumber producers in Canada.

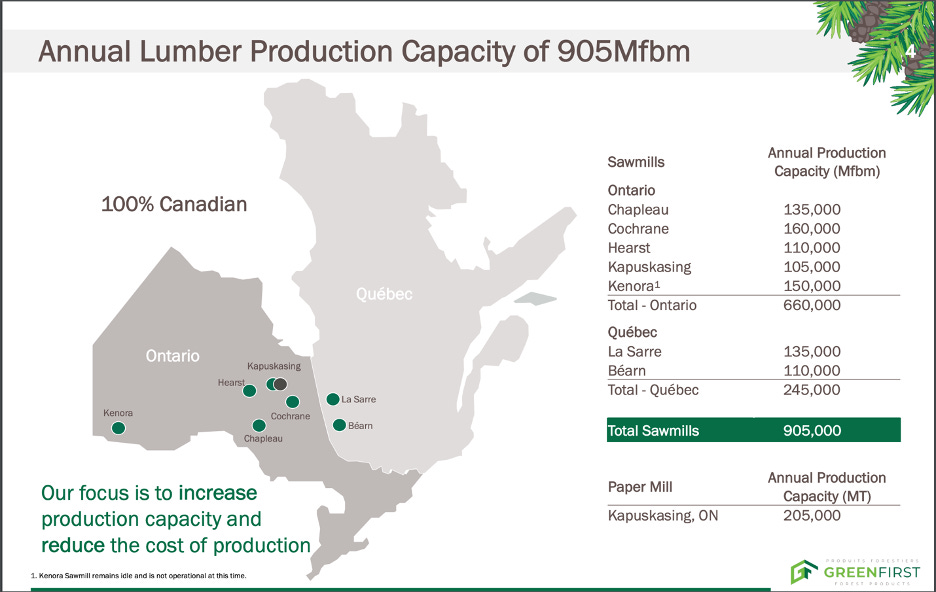

Today GFP owns 7 sawmills and 1 paper mill. Below is a helpful graphic from GFP’s investor presentation slides on each mill and its production capacities. (Mfbm = 1000 board feet)

Management has been adept and successful thus far, building GFP from essentially a pile of cash into an industry powerhouse. There is plenty of reason for optimism regarding GFP’s future given the skill of management and their clear growth plan: In GFP’s annual information form (customary filing in Canada), management stated they expect a large part of GFP’s growth to come from accretive acquisitions, key criteria for potential acquisitions are long term access to timber supply and long-term customer relationships for chips and other by-products. This plan plays to the strengths of GFP’s managers who are likely to continue executing.

Great. Management is adept. But the timber industry is extremely competitive - not to mention cyclical. The success of GFP will rely heavily on factors out of management control. Perhaps none of these factors will be more important than the price of Lumber. (Itself impacted by a variety of factors). Lumber has done well recently, futures as of writing are at 886.30/Mfbm. But these prices are well above historical averages. Until a recent boom, prices have floated between 200-450 Mfbm, as seen in the chart below:

Analysts and forecasters predict lumber prices to be volatile but remain above the historical trend. However, inflation is going to have a big impact in offsetting these strong prices. Inflationary cost pressures have already resulted in increasing stumpage rates, logging costs, fuel costs, and order delays. I would expect this to continue. The other two important factors in deciding future success for GFP, is, of course, supply and demand. Supply has been disrupted by COVID-19, while at the same time demand has been buoyed by a strong housing market. One can’t help but imagine those trends are likely to reverse – the Pandemic isn’t likely to get much worse, and housing is already showing weaknesses. I do believe though that GFP possesses some competitive advantages that should help insulate them from potential industry and economic troubles. In addition to the previously mentioned key agreements GFP acquired because of the Rayonier acquisition, the company also holds rights to access approximately 3.7 million m3 of guaranteed fiber supply across Ontario and Quebec. Fiber is important for supplying operating mills and the company stated they believe this supply is sufficient to support potential increases in lumber production capacity. Lastly, GFP is in close proximity to its biggest customers, reducing transportation costs, and they have built strong relationships with the local communities.

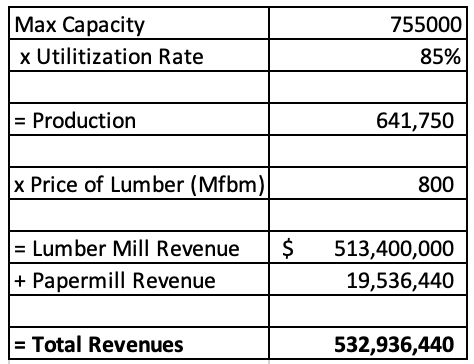

In fiscal 2021, GFP posted sales of $150m and COGS of $128m. It is important to remember that the acquisition of assets from Rayonier didn’t close until August 28, as a result, revenues are not at all reflected of what GFP should earn in a full year. In their 10-k the company states that had they completed the acquisition on January 1st, annual revenue would have been $504m. This lines up very well with what I estimated GFP would’ve sold in a full year with the assets, based on the price of lumber, their production capacities, and utilization rates:

(Utilization rate according to MadisonReport)

(Assumes papermill revenue remains constant)

Needless to say, this is an incredibly arcane method for predicting full-year revenues, but I believe it is reasonable, and more so it is useful for predicting future revenues. Using this method, I have estimated 2022 revenues to be around $635m. I am assuming lumber prices, paper mill revenues, and utilization rates stay the same, and I have increased GFP’s max capacity to 905,000 Mfbm to account for the Kenora Mill. (GFP is currently in discussions with the government to restart the mill)

Predicting revenues any farther out than 2022 is difficult given all the variables and the likelihood of more acquisitions that will increase max capacity. I believe though that my 2022 projections are a good representation of what GFP should hope to sell in the near-term future without any acquisitions.

Estimating operating earnings for 2022 and beyond is challenging, as we do not have any relevant historical data on GFP margins before 2021 (operating margins of 3%). Analyzing competitors is equally fruitless as the majority are private. There are a lot of sources online, but many are of dubious validity and do not cite where they got their info. Furthermore, most only collected data from American companies and reported no information for operating margins, only net profit margins (5-8%). Fortunately, I found that the Canadian Government has an industry statistics section on their website for Innovation, Science, and Economic Development (ic.gc.ca.com). Here I found that operating margins in the Forestry industry are 12.45% on average. For what it’s worth, this does line up well with the 14% operating margin that analysts predict for GFP in 2022.

Considering all the sources I looked at, 2021 margins, analysts’ predictions, my views on inflation, GFP’s competitive advantages, etc., I think 12% operating margins is a very reasonable target for the future. At 12%, 2022 operating earnings for GFP would be about $76m, or $0.43 per share (Analysts expect op. earnings of $89.23 or $0.50 per share). GFP has about $66.45m of debt, net of all cash, giving them an enterprise value of around $342m. That’s good for an EV/EBIT multiple of about 4.5x my predictions for 2022. In the Forestry industry EV/EBIT multiples tend to be low - around 6-9x (Data from Professor Damodaran’s site). To be conservative let’s take the low end of that range. 6x my expected 2022 EBIT, implies an enterprise value of $457m, and a market cap of $390.6m ($2.20/share). That’s about 42% higher than GFP’s current market value.

Thank you for reading, as always none of this is investment advice. Always do your own DD. I currently have no position in GFP .

Beautiful write-up. Currently, at Stage III of my DD and strongly considering investing. Thank you for your research.